How Personal Savings Affect the Economy

How Personal Savings Affect the Economy

Brett Klein | Partner | August 15, 2023

Despite the economic uncertainty of the past year, everyday individuals and households have been resilient. Consumer spending has remained steady in the face of high inflation, rising interest rates, housing market challenges, and layoffs in sectors such as tech. While it has helped that the recession anticipated by many investors and economists has not materialized, this fact is partially due to the strength of consumer finances. How do consumer balance sheets look today and how might this impact the economy and markets in the coming year?

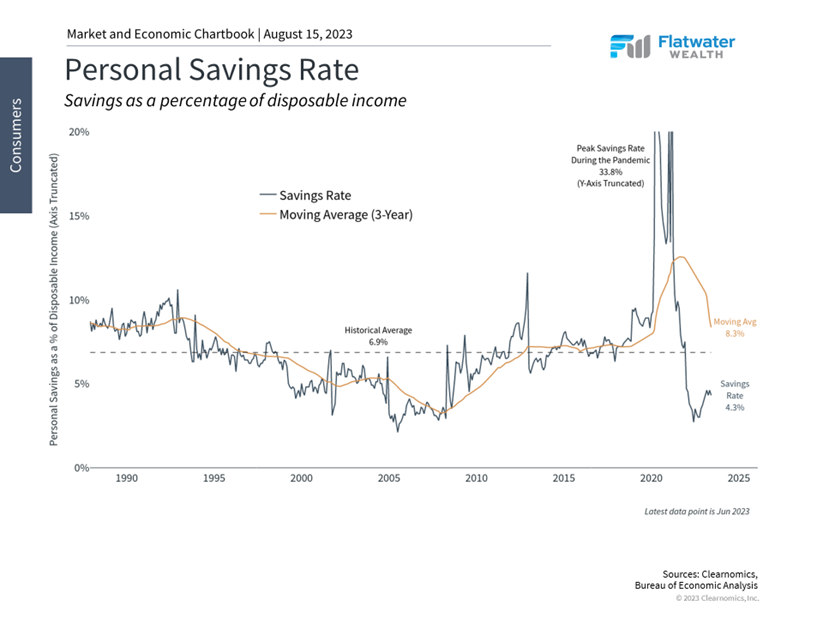

Personal savings have helped to cushion consumer finances

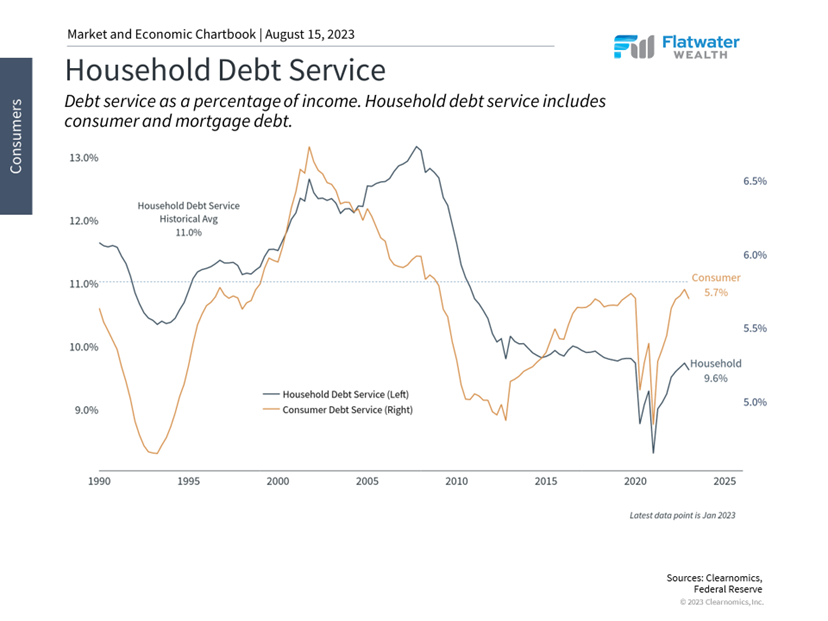

Household debt service has risen but is still historically low

Additionally, trends such as wage growth due to the strong job market could support both spending and savings. The latest report from the Bureau of Labor Statistics shows that wages rose 4.8% year-overyear. While this has generally been slower than inflation, hourly earnings are still rising at their fastest pace in 40 years. This is happening at a time when the national unemployment rate, at 3.5%, is near historic lows. Job openings have fallen to 9.6 million, but this still represents 1.6 openings per unemployed person across the country.

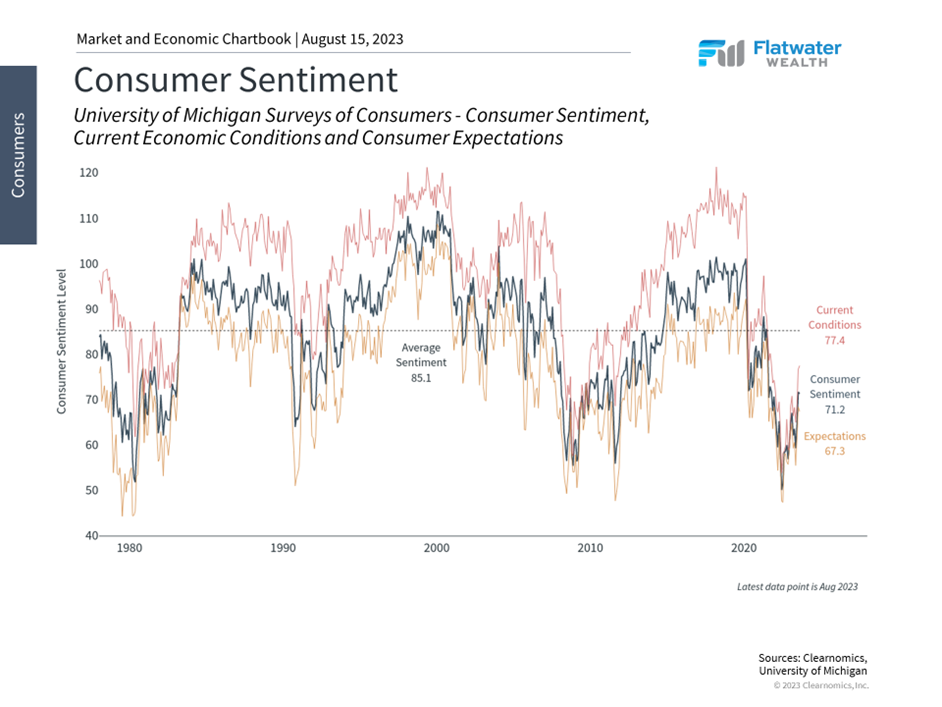

Consumer sentiment is only slowly improving

Of course, how consumers feel can differ from their financial pictures, especially as they look to the future consumer confidence, as measured by the University of Michigan Survey of Consumers, has suffered over the past year due to inflation and economic uncertainty. Fortunately, this is slowly improving as the economy stabilizes. According to the same survey, consumers expect inflation of 3.4% in the next year which could then decline to 3% over the next 5 years. While these represent high inflation rates, they are far better than what many had feared even just six months ago.

The bottom line? Consumers have been an engine of economic growth over the past three years. Although savings rates have fallen, the strong labor market and manageable debt service levels have supported consumer spending and the broader economy. From a financial planning perspective, investors should continue to save appropriately, ideally with the guidance of a trusted advisor, to achieve their long-term goals.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC. Flatwater Wealth is a sperate entity from LPL.

Copyright (c) 2023 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information an opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.